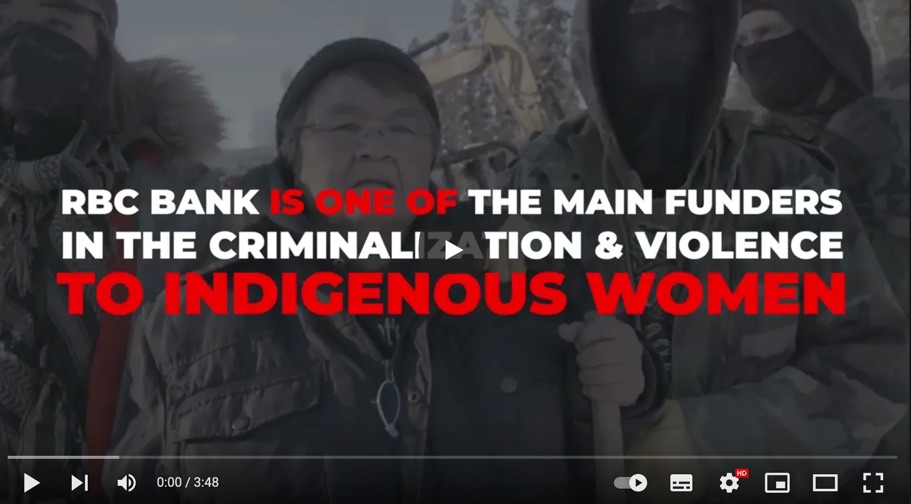

Coastal GasLink (CGL) is a dangerous project that blatantly violates Indigenous rights, and puts our climate goals at risk. Our partners Stand recently published a detailed case study on the problems with CGL.

Built by TC Energy, the 670-km Coastal GasLink pipeline is intended to carry fracked gas from Dawson Creek to Kitimat, BC, where it will be converted to liquified natural gas (LNG) for export to global markets. Despite unequivocal Wet’suwet’en opposition to the project, the pipeline runs through 22,000 square kilometres of the Nation’s unceded territory. It also crosses more than 206 ecologically sensitive waterways. The pipeline is built to carry 2.1 billion cubic feet per day of fracked gas, with a peak capacity of up to five billion cubic feet per day.

The Royal Bank of Canada (RBC) is among five commercial banks (including Bank of Montreal, Scotiabank, CIBC and TD bank) that provided the project with working capital. RBC provided CAD $275 million in project finance – including a co-financed $6.5 billion loan and a $40 million corporate loan, and $200 million in co-financed working capital – while acting as financial advisor for the pipeline.

RBC also holds over 85 million shares in TC Energy, which translates to about 8.6% of the company or more than a $1.03 billion-dollar stake (at $58/share). RBC not only finances TC Energy; it’s deeply invested in the company, and doubly exposed in the Coastal GasLink pipeline.

CNB, dubbed the “Bank of the Stars,” is a wholly-owned subsidiary of RBC, the lead financier of the Coastal GasLink pipeline. Since acquiring CNB in 2015, RBC has doubled down on fossil fuel financing, and is the world’s fifth largest fossil bank and Canada’s #1 fossil fuel financier.

The letter signed by actors, artists, athletes and musicians states, “Despite claiming to be a leader in climate conscious banking, since acquiring CNB in 2015, RBC has spent over $160 billion to become one of the world’s largest and most aggressive financiers of tar sands, fossil fuel extraction, and transport.”

“Our sacred headwaters, the Wedzin Kwa river, is the lifeline for our people. By financing Coastal GasLink, CNB’s parent company RBC is putting us profoundly at risk,” said Gidimt’en Checkpoint spokesperson Sleydo’, Molly Wickham. “The gas pipeline violates our hereditary title, and has led to years of RCMP violence and harassment of peaceful Indigenous land defenders, and the forced removal of Wet’suwet’en peoples from our territory. We’ve been crystal clear: RBC must divest from this toxic project, which threatens Wet’suwet’en land, air and water, and steamrolls Indigenous rights.”

With an estimated CAD $6.6 billion price tag, RBC is among top commercial banks providing the CGL project with working capital, including CAD $275 million in project finance, a co-financed $6.5 billion loan, a $40 million corporate loan, and $200 million in co-financed working capital – while acting as financial advisor for the pipeline.

“CNB and RBC have the opportunity to stand on the right side of history, and that starts with immediately divesting from Coastal GasLink,” said actor and activist Mark Ruffalo. “I’m heartened not only by the power of Wet’suwet’en land defenders, but also by my community of artists rising up to demand an end to all fossil fuel finance as we live through this climate catastrophe.”

“We refuse to allow our industry’s bank of choice to associate itself with the abuse of Indigenous Rights or to participate in accelerating the climate crisis,” said Alex Ebert, musician and composer. “Despite public statements, CNB’s parent company RBC is blatantly disregarding Indigenous peoples and our climate. This letter is not the beginning of this decade-long fight, or even close to the end. If CNB’s parent company doesn’t divest from its extreme fossil fuel extraction and transport operations, the ‘bank of the stars‘ will be known as the ‘bank of the tars’.”

In addition to Coastal GasLink, RBC is pouring millions into Russian oil and gas corporations, including one producing steel for the pipeline. The pipeline has been implicated in recent pushes to divest from Russian assets, as one of the main suppliers of steel to the pipeline is Russian-oligarch controlled Evraz.

“I spoke at RBC’s shareholder meeting in 2009 – RBC is not new to these tactics. They have been willfully financing destruction, including in my community through the tar sands, the dirtiest fossil fuel in the world,” said Melina Laboucan-Massimo, Senior Director, Indigenous Climate Action. “Bankrolling Coastal GasLink is just the latest example of RBC covering up their role in violating Indigenous rights, not upholding free, prior and informed consent as outlined in UNDRIP, and in exacerbating the climate crisis. In my community, we can’t drink our water because of RBC’s investments. We want to make sure Wet’suwet’en communities still can.”

Today RBC released – to little fanfare, and deservedly so – an update on it’s ESG activities. Included in the update were next steps on its climate plans, as part of their participation in the Task Force on Climate Related Disclosures.

Investors for Paris Compliance, an investor advocacy group tracking climate policies at RBC and others, released this statement:

RBC is falling behind in its efforts by failing to set 2030 targets for carbon-intensive sectors and by omitting the majority of its financed and facilitated emissions, contrary to its Net Zero Banking Alliance commitments and best practices. There is no attempt to address recent controversies regarding RBC’s financing of fossil fuel projects that violate Indigenous rights, nor to end financing of fossil fuel expansion in accordance with the Net Zero scenario of the International Energy Agency.

Said Matt Price, Director of Corporate Engagement with Investors for Paris Compliance (I4PC): “Today RBC failed to change course as Canada’s largest funder of fossil fuels with a go-slow approach in the face of the climate emergency. By not setting 2030 targets and underestimating its financed emissions, the bank is falling behind its competitors, which is disappointing to investors.”

As world governments and corporations push back against Putin’s aggression by pulling out of Russian business, many financial giants and investors don’t seem to have a problem propping up Putin’s war machine.

As reported in the National Observer, a new report from Stand highlighted holdings in Russian oil, gas, and coal companies by global investors. Canada had many investors on the list, including RBC.

New research from international climate non-profit Stand.earth shows Manulife, RBC, CIBC, BMO and others have collectively financed Russia’s three largest oil and gas companies — Gazprom, Lukoil and Rosneft — with more than US$110 million worth of investments. The data was compiled using financial software called a Bloomberg terminal that tracks investments in real-time.

According to the data, RBC owns $6.3 million in shares of Lukoil and over $31 million worth of bonds from Gazprom. Similarly, BMO owns $4.3 million worth of shares as well as $3.3 million worth of bonds in Gazprom. CIBC holds $7.8 million worth of shares in Lukoil and just over $240,000 worth of shares in Rosneft.

Other financial institutions supporting the Russian oil and gas giants include AGF Management, MD Financial Management, Sun Life Financial, Desjardins Trust, Fidelity Investments Canada, 1832 Asset Management and Power Corp of Canada.

Stand.earth climate finance director Richard Brooks told Canada’s National Observer that even if the total figures aren’t enough to fundamentally change the calculus of the invasion of Ukraine, these institutions should divest themselves as part of the Canadian response to Russia, from symbolic actions — like lighting up the CN Tower in Ukraine’s colours to other economic tactics like sanctions.

“The investment isn’t in the billions of dollars, but that doesn’t mean Canadian financial institutions are off the hook in terms of taking responsibility for where their money is being invested and what kind of activities their money is supporting,” he said.

“If Vladimir Putin didn’t have Russian oil and gas revenue, then he wouldn’t have been able to amass the war chest that he has to be able to invade Ukraine,” he added.

This week, Greenpeace Canada released the Money Can’t Buy Our Love report with the Canadian youth-led organization Banking on a Better Future. The report highlights marketing techniques used by the top five Canadian banks (RBC, TD, Scotiabank, BMO and CIBC) in philanthropic ventures to draw in young customers.

As reported in Toronto’s NOW Magazine:

Banks have long mounted impressive branding campaigns to highlight their support of arts and cultural organizations. Their logos and financial might are now increasing behind campaigns on university campuses and high schools.

But banks are profit-driven institutions, and while posing as philanthropists, their contributions also distract us from the very real harm these institutions cause through their financing of fossil fuel projects that pump climate chaos and violate Indigenous rights. Banks are putting their reputation at risk with youth by continuously betting on destructive fossil fuels.

Except, $50 million a year is a trickle compared to the $208 billion in RBC financing directed to new fossil fuel expansion projects since 2016, which earns it the title of Canada’s largest fossil fuel funder. The disparity is shocking.

Despite Canada’s commitment to phasing out thermal coal electricity within eight years, Canadian banks are continuing to lend and invest more than USD$100 billion (CAD$127.23 billion) to coal-related companies, including in Canada, according to a new report out of Germany that tracks investment information on thermal coal from 600 financial institutions worldwide.

The findings, from Urgewald, also show that RBC is one of Canada’s biggest backers of thermal coal, with almost USD$11 billion (CAD$14 billion) of lending and financing to coal related companies, and holding USD$6.5 billion (CAD$8.3 billion) in bonds and shares.

“While communities across Canada and around the world experience devastating climate impacts from fires to floods, Canada’s fossil banks continue to finance coal-related companies to the tune of roughly $100 billion. In 2022, RBC financing fossil fuels while spouting sustainability is like handing out cigarettes while warning about the dangers of smoking,” said Richard Brooks with Stand.earth. “From financing coal, the dirtiest fuel on the planet, to greenwashing attempts, to financing Coastal GasLink’s violence against Indigenous land defenders, RBC finds itself on the wrong side of history. Time for RBC to drop coal exposed companies and phase out financing of oil and gas.”

Urgewald’s findings show that RBC is the only financial institution in Canada to make the top three of both Canada rankings in lending and investing in coal related companies.

Lending & Underwriting of Canadian banks to GCEL 2021, in million USD (2019-21)

Loans

Underwriting

Total

Non-Canadian Companies

USD 20,326

CAD 25861.68

USD 21,068

CAD 26805.76

USD 41,394

CAD 52667.45

Canadian Companies

USD 4,773

CAD 6072.90

USD 3,531

CAD 4492.65

USD 8,304

CAD 10565.55

Coal Related Companies

USD 2,969

CAD 3777.59

USD 2,097

CAD 2668.11

USD 5,066

CAD 6445.70

Coal Related Companies – RBC

USD 609

CAD 774.86

USD 444

CAD 564.92

USD 1,052

CAD 1338.51

Bond- and Shareholdings of Canadian investors to GCEL 2021, in million USD (Nov-21)

Bondholding

Shareholding

Total

Non-Canadian Companies

USD 7,473

CAD 9508.23

USD 31,354

CAD 39893.11

USD 38,827

CAD 49401.34

Canadian Companies

USD 2,371

CAD 3016.73

USD 9,509

CAD 12098.73

USD 11,880

CAD 15115.46

Coal Related Companies

USD 9,844

CAD 12524.96

USD 40,775

CAD 51879.87

USD 50,619

CAD 64404.83

Coal Related Companies Developers – RBC

USD 1,203

CAD 1530.63

USD 5,379

CAD 6843.94

USD 6,582

CAD 8374.57

The Global Coal Exit List is maintained by Urgewald. It is the most comprehensive list of coal related and coal exposed companies in the world and relied upon by more than 600 financial institutions to inform their financing and investment of energy sector companies. More info can be found at: https://coalexit.org/about-us

See more photos from this action at RBC’s Toronto headquarters here.

A new report out this week by a European NGO tracks how banks continue to fund the expansion of fossil fuels, even after signing onto Mark Carney’s high profile Net Zero Banking Alliance last year.

Why is this a problem? All of the climate science projections and even the International Energy Agency’s most recent energy analysis shows that the planet can afford no new fossil fuel expansion while keeping global warming to under 1.5 degrees C. The expansion simply must stop.

But banks are clearly not getting the memo. Kate Aranoff, writing in the New Republic this week, summarizes:

A new report from the U.K.-based charity ShareAction finds that 25 European NZBA members have provided at least $38 billion in financing to 50 of the most expansionary upstream oil and gas companies on earth. Half of that financing was provided by four of the founding signatories of the Alliance: Barclays, BNP Paribas, Deutsche Bank, and HSBC. Since the Paris Agreement was brokered in 2016, the European banks analyzed have furnished upstream oil and gas expanders with $400 billion, and they “show no signs of stopping”.

She goes on to report:

Just as European oil companies have been quicker to announce net-zero pledges than U.S. companies, European banks have generally been more forthcoming with climate commitments. But talk doesn’t always translate to action: Just five of the European banks analyzed have begun to restrict financing for oil and gas projects, while only one—La Banque Postale—has a defined phaseout plan, to exit the oil and gas sector by 2030.

Others have been more canny: Barclays, for instance, pledged to cut off financing for shale drilling in Europe and the U.K. but not the U.S. “It’s a trend with a lot of bank policies,” Shields said of the Barclays pledge. “They have great headlines to go out with, but once you drill down into the policies, you see these big exceptions. A huge number of those exceptions allow them to continue business as usual.”

While the report is focused on European banks, Canadian banks – who joined Carney’s Net Zero Banking Alliance all at once and right at the last minute before the Glasgow COP – are even worse at funding expansion. Expect new numbers from RBC and the rest of the dirty Canadian banks next month when the latest Banking on Climate Chaos figures are out.

Financial reporter Shawn McCarthy spent many years at the Globe and Mail, and has recently moved to Corporate Knights to cover sustainability issues. His recent article highlights how investor and public pressure is growing on banks – especially RBC – to deliver on vague net zero promises by drawing the line at financing further fossil fuel expansion.

Under the Glasgow Financial Alliance for Net Zero forged for COP26, the banks have committed to not only decarbonize their portfolios but to adopt a transparent and rigorous short-term strategy that ensures they meet that 2050 target. The alliance, led by former Bank of England governor Mark Carney, comprises separate agreements for various financial sectors.

The banking agreement includes many of the largest financial players in North America, including JPMorgan Chase, Citigroup Inc., Royal Bank of Canada and Toronto-Dominion Bank.

The article highlights investor groups who are also building up pressure to make clear short term financed emission reduction targets:

Civil society research groups in the United States and Canada are determined to hold the industry’s collective feet to the fire. On December 16, Investors for Paris Compliance, a Canadian advocacy organization, released a “best practices” report that aims to guide not only banks but their shareholders, who are increasingly challenging business-as-usual practices at annual meetings.

The report calls on banks to put in place policies that will allow them to cut the carbon emissions of companies they finance by half by 2030, and to immediately end financing for new fossil fuel projects. The banks should adopt science-based targets for 2030 – aligned with the goal of limiting the average global temperature increase to 1.5°C above pre-industrial levels – and tying compensation to progress on meeting the climate goals.

The report notes that the world is already seeing enormous costs from extreme weather events related to climate change, most recently with the catastrophic flooding in British Columbia and the searing heat and drought experienced throughout western North America last summer.

The news that RBC is Canada’s #1 climate-killing financial institution is catching on across the country. This week a man in Orillia, Ontario, part of the local XR GTA chapter, brought a message about extinction right to his local RBC branch:

A man who goes by Xavier Bergeron, an alias used to protect his identity, says he, accompanied by a photographer and videographer, was protesting RBC Royal Bank’s involvement with the fossil fuel industry.

“We went inside the bank, we were asked to leave, but I told the manager I refuse. She threatened us to call the police and I told her to go ahead, we will be outside waiting,” Bergeron told OrilliaMatters.

Bergeron, 54, says the protest was peaceful and the protesters were following all COVID protocols.

“While waiting for the police, I chained myself to the front door to make a point and resist arrest, as well as showing how I feel about the financial institution’s financing of ecological breakdowns,” he said.

“We all know that fossil fuel is bad, and the science is undeniable now. Levels of carbon dioxide in the atmosphere are getting dangerously close to the tipping point where we will no longer be able to grow crops,” he said.

“It’s going to trigger sea level rises which will cause a billion people to be on the move,” he said.

Amidst the ongoing COVID-19 pandemic, this past year’s impacts of intensifying climate change from floods to fires have hit Canadians hard, costing our health-care system billions, demolishing infrastructure and roads, and immeasurably impacting communities’ lives, livelihoods, and traditions.

In the face of this climate emergency, we are seeing hopeful developments in growing public awareness of who’s responsible, including the role of the financial sector. While Bay Street and Wall Street remain a hotbed of problems (more on that in a moment), this year we marked a massive milestone, noting a decade of progress for the fossil fuel divestment movement with 1,500 institutions representing nearly US$40 trillion in assets committing to no longer invest in coal, oil, and gas companies causing climate destruction. And just this month, Laurentian Bank, Canada’s seventh-largest bank, announced its commitment to end fossil fuel finance.

Yet as our society transitions off fossil fuels and institutions take action to clean up their pools of money, too many banks, insurance companies, and institutional investors like pension funds continue to be great enablers of climate change. Canada’s pension funds have been doubling down on carbon-intensive portfolios, investing in toxic fossil fuel infrastructure, and even have board members with controversial ties to the oil and gas industry.

Our big banks are no better. As the fifth-worst offender in the world, RBC has financed more than $200 billion in fossil fuels since the Paris Agreement was signed, including in the Coastal GasLink pipeline. The real-world impacts and conflicts these investments generate are being exposed right now as Coastal GasLink violates Indigenous rights in Wet’suwet’en land, including militarized police raids in B.C, and faces million-dollar fines for repeated environmental infractions.

In a quickly warming world, most Canadian banks and pension funds risk being laggard outliers. With occupations and dozens of arrests at RBC branches across Canada in solidarity with land and water defenders, pressure is escalating on Canadian banks to stop the money pipeline to fossil energy companies.

In a quickly warming world, most Canadian banks and pension funds risk being laggard outliers. Photo by Morgan Sharp / Canada’s National Observer

Canadian fossil finance fails — and climate wins — in 2021

March: The 2021 Banking on Climate Chaos report from Rainforest Action Network, the Indigenous Environmental Network, and more reveals Canada’s big banks consistently rank as top 20 fossil bankers, with RBC as the country’s worst offender and a top financier of tar sands.

April: A climate shareholder resolution at RBC garners 31 per cent support, laying the groundwork for a 2022 resolution to stop fossil fuel expansion and affirming shareholders are paying close attention and concerned with management.

November: The Glasgow Financial Alliance for Net Zero (GFANZ) launched with hope in the spring, but by COP26, banks were using it as a greenwashing cover rather than a space to address the inevitable end to fossil finance and investments in climate solutions.

December: Bloomberg reporting reveals all major Canadian banks signed a slew of loan and bond deals with fossil fuel companies in 2021, despite net-zero rhetoric. In contrast, Laurentian Bank announces its commitment to end fossil fuel finance, differentiating itself from the other big banks.

Looking ahead to 2022

As climate impacts intensify, Canadian banks remain fossil fuel companies’ go-to lenders. Much ballyhooed net-zero rhetoric, joining alliances like Mark Carney’s GFANZ are wearing thin, and people are clueing in on the role these banks play. The banks have played a role in holding back more effective climate action in Canada and bankrolling extreme weather events that grabbed headlines and affected millions this past year.

In 2022, we’ll see more customers, shareholders and politicians questioning the role of finance, and taking actions from moving money and voting their shares or exploring regulatory actions, to demanding accountability and meaningful action from Canada’s biggest banks and pension funds. The crystal ball remains unclear how our financial institutions will respond: with real transparent action or more deflection and defensiveness. Time’s running out, I hope they chose the former.

Richard Brooks is the climate finance director with Stand.earth